A Look at the Stock Market, the Value Premium and Crypto Prices in 2022

Note: None of this constitutes investment advice, so please do not take it as such.

There is a running joke amongst academic economists that many people will ask them what stocks they should buy, despite the fact that their research has absolutely nothing to do with finance whatsoever. Since my work focuses on asset pricing in part, I do not have this excuse. A typical, albeit not very exciting, answer to this question is "buy a broad-based index fund and don't try and pick individual stocks". The reasoning behind this is that a wealth of research finds that it is essentially a fool's errand to try and systematically identify which assets will do well and won't unless you have some kind of relevant information available to you which other investors do not have access to. All other readily available information should already be 'priced in', and so it is not possible to gain any kind of edge and beat the market on a risk-adjusted basis by using it, and consequently you should just try to diversify as much as possible while minimising your fees. This is the strong form of the highly influential efficient markets hypothesis, developed by Nobel prize winner Gene Fama, and the subject of the well-known book 'A Random Walk Down Wall Street' by Burton Malkiel. Whether or not the efficient markets hypothesis holds, in reality, is debatable, and long-debated it has been, but I think it is definitely a good approximation to reality, although probably not in its strongest form. The Capital Asset Pricing Model (CAPM) of Sharpe, Markowitz and Miller is a closely related idea and essentially states that the average return an asset earns should only depend on how correlated it is with the aggregate market return. Assets which covary strongly with the market portfolio (high beta assets) are risky and so earn higher returns via a risk premium, while assets that move in the other direction to the market (negative beta assets) provide hedging benefits, and so earn lower expected returns. The expected return on asset j should be given by:

Where the alpha term should be zero for all assets. These two ideas provided the core of the first revolution in finance during the 1960s and 70s. Much work since then has been devoted to looking at how and why they do not hold entirely. Many CAPM anomalies have been documented, and some are likely just the result of chance or fishing for statistical significance by researchers, but one that seems to be much more robust over time is the value premium. This refers to the empirical tendency for value stocks – stocks that have a high ratio of their book value to their market value – to consistently earn higher returns than the CAPM would predict. Note that this is just one measure of value, others include things like the price/earnings or price/dividend ratio, but they all capture the same concept – these stocks are cheap relative to a measure of their 'intrinsic' value. Why it is that the value premium exists is a little unclear, with some favouring a behavioural explanation (i.e., it is due to some kind of bias amongst investors) while others have argued that the higher returns represent genuine risk premia as value stocks are more exposed to risk factors that investors care about, like inflation for example. The figure below plots the annual return on the high value minus low value (HML) portfolio of Fama and French since 1927 from the US. If I regress the high minus low return on the market return, the alpha term is positive and statistically significant, meaning that the value return is not entirely explained by the CAPM and there seems to be an anomaly present.

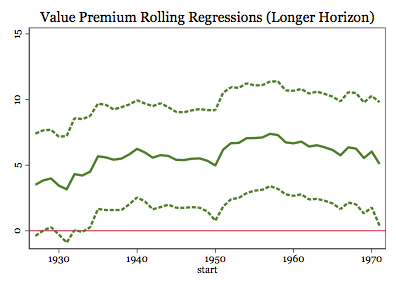

What are the implications of this for investors? Well, it would seem as if value investing offers a source of slightly higher risk-adjusted returns (the estimate of the intercept in the full sample implies that this value portfolio offers 3.41 percent additional risk-adjusted returns per year), and indeed it has been viewed this way for long before the 1970s. In Benjamin Graham and David Dodd's seminal 'Security Analysis' published in 1934, they essentially make the case for buying stocks that are trading at discounts relative to their book values. Warren Buffett is also a famous advocate of value investing. As always, however, it is not an unequivocal free lunch. In the graph above, you can see that the value premium is very volatile over time. I run rolling CAPM regressions of the HML return on the market return with a fixed 20 year period, plotting the estimates of the resulting alpha along with its 95% confidence intervals. For most of the windows, we cannot reject the null hypothesis that the alpha is zero. Furthermore, value has been taking a bit of beating since the turn of the millennium. You can see this in both of the two graphs. The fundamental reason for this has been the dominance of the MAGFANT (Microsoft Apple Google Facebook Amazon Netflix Tesla) types of stock in recent years. These types of stock are labelled growth stocks, and they are the antithesis of value stocks as they typically have a very low book-to-market ratio. They are labelled growth stocks since their value derives from expected cash flows relatively far in the future. For a very long time, Amazon was operating at a loss for instance, but investors were pricing in substantial expected future profits and hence their share price was high. These types of stocks are a lot sexier than value stocks since value stocks are often companies that have a history of success but do not have clear growth upside going forward. Perhaps this partially explains why some are less keen to invest in value.

The poor returns of value over the last 20 years have led some to question whether the value premium is dead, but I am not convinced of this. Conversely, my expectation would be for the value premium to re-emerge going forward. Firstly, after four tough years for value previously, it bounced back in 2021 with an annual return of 17%, albeit in a good year for stocks with an annual return of 18% for the market. Secondly, if we take a longer horizon of 50 years in our rolling regressions, the value premium is present almost ubiquitously. So over the longer term, value does seem to robustly earn positive risk-adjusted returns. This is basically another way of saying that it has displayed a remarkable tendency to bounce back after rough patches, and I do not see a good reason why this time is different. Thirdly, if we are indeed moving to a higher inflation, higher interest rate environment as I believe we are, the advantage of growth stocks should be eroded to some degree. As I mentioned previously, growth stocks typically are not profitable now but are expected to be in the future, sometimes not for quite a long time. An asset's price is given by its expected, discounted sum of future cash flows, and so cashflows that accrue further in the future are subject to more discounting. The duration of an asset is the weighted average of its cash flows and as such measures the time horizon at which the asset's cash flows accrue. Growth stocks are high duration assets akin to long-term bonds, while value stocks are low duration assets. Another property of duration is that it gives the sensitivity of an asset's price with respect to interest rates. As a result, the price of growth stocks should be sensitive to changes in the path of monetary policy, with increases in bond yields associated with decreases in the price of these assets. When I regress the weekly HML return on the weekly change in the 10-year yield using data from post-2000, I get a positive and statistically significant coefficient. So it is indeed the case that higher expected future interest rates push the price of growth stocks down relative to value stocks, meaning the return on the HML portfolio increases. If you believe that further monetary policy contraction is on the way, then this likely also implies that value will perform relatively well going forward. As this excellent blog post details, high duration stocks (including growth stocks) have been going gangbusters since the start of the pandemic, potentially as a result of how expansionary monetary policy has been. During the Fed's tightening phase of Oct 2017 to Feb 2020, the opposite was true with low duration stocks (such as value stocks) outperforming high duration stocks by a very large degree. An even stronger tightening cycle looks to be necessary now, and this creates a bullish case for low duration, value equities.

The last few weeks in the stock market have been rocky, to say the least. Monetary tightening hurts stocks in general since they are high duration assets relative to others. An interesting occurrence has been the accompanying decline in crypto prices. Some proponents of crypto have argued that it draws some of its value from providing hedging benefits against equities. If we run a CAPM regression of the weekly Bitcoin return on the weekly market return, we get a beta of 0.8, implying that it is very strongly correlated with the aggregate stock market and that the previous claim is demonstrably false. The intercept in this regression is positive and statistically significant, so the correlation is not strong enough to fully explain its excess returns. Following the discussion above, a natural question to ask is what duration Bitcoin exhibits. Regressing its returns on the change in the 10-year yield again gives a positive, quite large and significant coefficient, implying that in practice Bitcoin behaves like a high duration asset and is very sensitive to the path of interest rates. I say it behaves like rather than is a high-duration asset because duration is time-weighted cash flows, of which Bitcoin has none. These two empirical features documented here can help to rationalise the crypto crash we have seen, and possibly hint at a prolonged reversal if the Fed does hike rates quicker than the market is currently expecting.

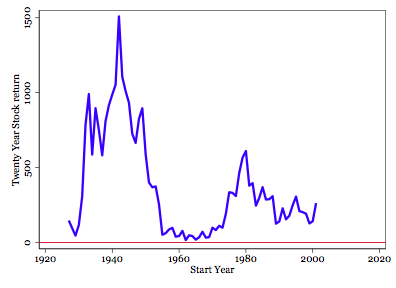

When I do get asked for stock recommendations, my answer is " buy a broad-based index fund, don't try and pick individual stocks, and consider tilting towards value ". Still pretty dull but not as boring as it could have been, I suppose. The key to investing in stocks, though, is patience and a long investment horizon. The S&P 500 is down about 10% this month, and while this is a large drop, it is really not that uncommon. Since 1927, there have been 33 months featuring a drop at least that large, meaning on average it happens about once every three years. Bad years are also far from uncommon, with a 10% yearly drop happening roughly one year out of every five. Bad twenty-year stretches are practically unheard of though. In fact, if you had invested in the US stock market with a twenty-year horizon during any period, you would never have lost money. On average your investment would be worth 470% of its original value, and even during the worst possible stretch between 1962-1982, you still would have made a 17% return. With monetary policy set for a much-needed tightening, it is likely that stocks, particularly growth stocks such as tech companies, as well as crypto, may be in for a rough time in the short run after an unbelievable two years and longer. This makes value stocks an interesting proposition, as well as other low duration assets. In the longer run, stocks remain a very good bet, as they always have done.