Is Inflation a Problem in the UK?

A return to the 1970s is unlikely, but some are far too blasé about the problem.

UK inflation has risen above 3%, which is something I would have only been able to say two times previously in my lifetime. For those below the age of 40 in fact, inflation has not been a first-order problem, with the average inflation rate standing at about 2% during this time. The reasons for this are numerous: more scientific monetary policy, a general weakening of demand (e.g. the slow recovery after the 2007-09 recession) and reduced volatility of oil prices to name a few.

Those above the age of 55 or so, however, can probably vividly recall what periods of high inflation look like. In the 1970s the inflation rate gradually crept up to a peak of an eye-watering 25%. Indeed the average rate during this decade was 14% — barely fathomable to us millennials. It got so bad that in a desperate attempt to cut costs, publishing houses started printing shorter books in smaller font. Eventually, they gave up with printing the price on the books as this was a fool’s errand, and instead opted to use post-it notes. In the US, things were just as bad and it eventually took the no-nonsense figure of Paul Volcker, who became chair of the Federal Reserve in 1979, to get a handle on it by raising interest rates substantially. This was far from painless, however, as it came with a side effect of a deep recession and high unemployment for the first half of the 1980s. As such it is natural to ask the question: should this return to high inflation rates be viewed as a cause for concern, or merely a temporary annoyance that will dissipate as soon as it materialised?

A large contingent of economists and commentators have insisted that this rise in inflation is largely a product of growing pains that have emerged from the global economy restarting after 18 months of lockdowns and the many other effects of the pandemic. Supply chains are incredibly complex in the modern economy, and these disruptions were largely inevitable. Commodity prices have shot up, with the global commodity price index increasing by 68% year-on-year. There has been a shortage of many types of workers who are important in the logistical aspects of transporting and distributing goods, causing firms to be forced into offering higher wages in order to attract enough of them. Talk about wages more and show graph. For example in the UK, there has been a well-documented shortage of HGV workers that has been exacerbated by Brexit, although this is not the proximate cause as the US are experiencing a similar shortage. Higher wages and higher input costs unsurprisingly cause firms to put their prices up, which leads to a rise in inflation. This is the typical supply shock story, and if you believe it you will probably also believe that these issues will resolve themselves soon, which will cause inflation to swiftly revert back to the Bank of England’s target rate.

To me, the ‘team transitory’ argument makes several important points, and I think on balance I agree that inflation is unlikely to remain elevated for a very prolonged period. This being said, there are other factors that give me more hesitancy and I think many are being too relaxed about the inflationary threat. The Phillips curve is an old concept in macroeconomics that basically explains the relationship between unemployment (or real GDP) and inflation. The old Keynesian version basically says that when demand is strong in an economy, unemployment is low which gives workers more bargaining power to demand higher wages, which in turn pushes up inflation. The New Keynesian version, which is typically used in the types of models used by central banks, features a very similar logic but also stresses the role of inflation expectations. The mechanism here is, essentially, that if firms and households expect higher inflation next month, they will set higher prices/demand higher wages which increases inflation today. We can write the NKPC as follows:

Where Pi is inflation and Y is output and the E part denotes people’s expectations that they make today. The t subscript represents today while t+1 represents the next period. There is an additional term, Z, that acts as a supply shock of the variety described previously. There has been a number of research papers recently that have found that the slope of the Phillips curve is likely to be very flat, I.e. kappa is close to zero. This tells us that demand-side inflation is not likely unless unemployment is very low indeed, which it is not in the UK by any means. Therefore, supply shocks are a more likely source. This is certainly true, but also neglects the role of long-run expectations. The NKPC equation can be re-written in the following form as in Hazell, Herreno, Nakamura and Steinsson (2021):

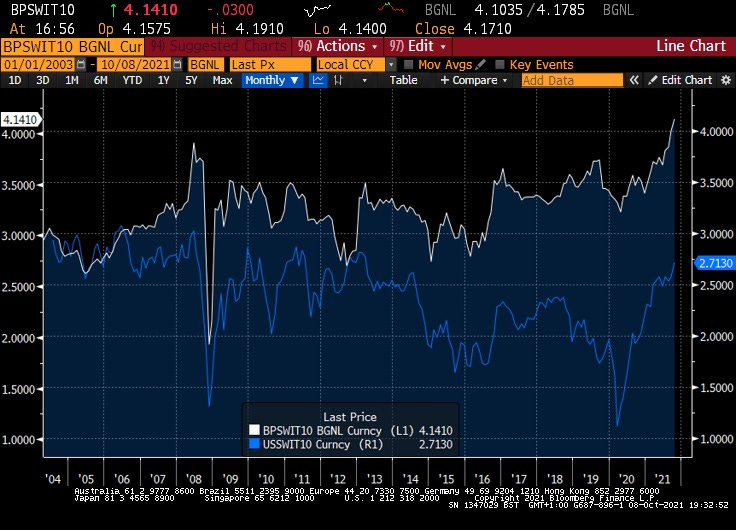

This tells us that the long-run expectations about the rate of inflation are a crucial determinant of inflation today. If people start to believe that the Bank of England is not serious about their inflation target, they price this in and inflation increases. These expectations should not be affected by short-term supply shocks and instead can be thought of as representing beliefs about monetary policy. What is the data telling us about this? The figure below plots 10-year inflation swaps for both the UK and US. This is essentially a market-based measure of what inflation is expected to be in the long run, and we can see that it has crept up to above 4.1%, suggesting long-run inflation expectations have increased. However, one can see by looking at the evolution of the series that it has consistently been around 3%, which is higher than inflation has actually ended up being. Since it is derived from an asset price, it may also feature a risk premium, meaning that it gives risk-adjusted inflation expectations which can differ from actual expectations. Nonetheless, an increase likely tells us that long-run inflation expectations have risen.

The best way to restore confidence and push these back down again would be for the Bank of England to signal that it is serious about keeping inflation close to its 2% target level. It certainly does this in its communication, but talk can be cheap and an interest rate rise may be the only way for markets to take them seriously. Indeed it seems that markets are now expecting a rate rise in December. This will almost certainly be followed by some unwinding of their QE program, as it has bought £900bn of UK government bonds. The problem with taking these steps is that it will likely stifle demand in the economy, and potentially impede the economic recovery from the pandemic. The UK has an output level further below its pre-Covid trend than any other G7 country and so this is obviously not ideal.

It is a difficult balancing act between inflation and unemployment that a central bank has to navigate in a situation such as this, and while I can see both sides of the argument I would ultimately think a rate rise is a good idea. My reasoning for this is that failing to do so early may necessitate larger rises down the road. At a certain point, markets may lose faith in the ability of the Bank of England to do what is necessary to bring inflation down - ask yourself how politically tolerable the kind of recession which was necessary under Volcker would be today. Sending the signal via a swift, decisive rate rise is likely to alleviate this to a large degree, and this is ultimately why I expect inflation to be transitory. If all goes well, the supply shock part of inflation will dissipate and it will go back down, giving the Bank more scope to think about providing economic stimulus in the future. A combination of factors has meant that the UK is not in a great position — ideally, we would be a lot closer to the pre-pandemic level of output before a monetary tightening. A slow recovery is painful, but not as painful as inflation expectations becoming unanchored, and it is probably best to act early, perhaps earlier than one would like, in order to stop inflation going from an annoyance to a disaster. Hopefully, the books which will be written on the post-pandemic economic response do not have to devote many passages to the inflation that followed. And hopefully, their prices are printed on the back and not written on a post-it note.