The Disconnect Between Economists and Popular Personal Finance Gurus

The Disconnect Between Economists and Popular Personal Finance Gurus

Plus My Year-end Top 10 Lists

An undeniable fact is that economists often have far less influence in the field they work in than non-economists. A clear case of this comes in the form of personal finance. If you go to any Waterstones and head to the economics or business section, the array of personal finance books will likely be written entirely by practitioners, entrepreneurs or businessmen rather than professors. For example, Robert Kiyosaki’s book Rich Dad, Poor Dad has sold over 41 million copies worldwide since it was published in 1997, while a swathe of personal finance podcasts such as The Dave Ramsey Show and The Clark Howard Podcast get millions of listeners each episode. On the contrary, I doubt many regular people have heard of Robert Merton, who solved the classic portfolio allocation problem in 1969 and was instrumental in the genesis of household finance as an academic field. The approach taken by economists is, perhaps unsurprisingly, very different to that of the typical personal finance guru and often looks something like this:

An economist typically writes down and solves a model for the relevant household finance problem, be it how much to invest in stocks vs bonds, how much to save and consume, what type of mortgage to get etc. Personal finance writers typically prescribe a set of heuristics that are widely applicable and akin to a philosophy of how an individual should approach their financial affairs.

A natural question to ask is how similar the popular finance advice is to the optimal decision rules that come out of an economic model. This is exactly what James Choi does in a very nice recent paper in the Journal of Economic Perspectives. Interestingly, there are several points on which the two approaches are not aligned (as well as several others where they are). It is worth noting at this point that I don’t believe that economists are always right and personal finance gurus wrong when there is a point of contention, and often how people actually behave can tell us some very useful things about what factors the models might be omitting.

Two Interesting Points of Disagreement

1) Consumption-saving rules

A famous result in economics states that households should smooth consumption over their life cycle, i.e. try to consume roughly the same amount at all points of their life. The logic behind this is that households are risk-averse with a concave utility function, meaning that they have an aversion to consumption volatility and dislike large period-to-period fluctuations. In other words, a consumer would much prefer to consume £400 of food in January and £400 worth in February rather than £100 in January and £700 in February. Extending this logic yields the consumption-smoothing result. In the most extreme form, it implies that a household should calculate the expected path of their lifetime income and use this to create a smooth path of consumption, borrowing if necessary to deal with periods such as early in life when income is likely lower than what it will be later in life. In reality, borrowing capacity is constrained and this is a very natural extension to the benchmark model that leads to weaker consumption-smoothing. Other additional frictions include risky labour income, habits in consumption and many others. Ultimately, despite these, consumption-smoothing to some extent remains desirable.

Personal finance authors typically find this approach baffling, instead prescribing a savings rule that does not vary much by age or income. A common recommendation is for an individual to save something like 10-15% of their income. The logic they often use to advocate this approach combines three things. First, they argue that saving is a skill that needs to be honed over as much time as possible, meaning that it is imperative to start saving when young. Second, they argue in favour of simplicity, with the simple savings rule obviating the need to perform the complicated arithmetic that would be necessary to even approximately solve a mathematical consumption-savings problem. Finally, compound interest is often emphasised as a powerful force, but this is also taken into account in the canonical consumption-savings model.

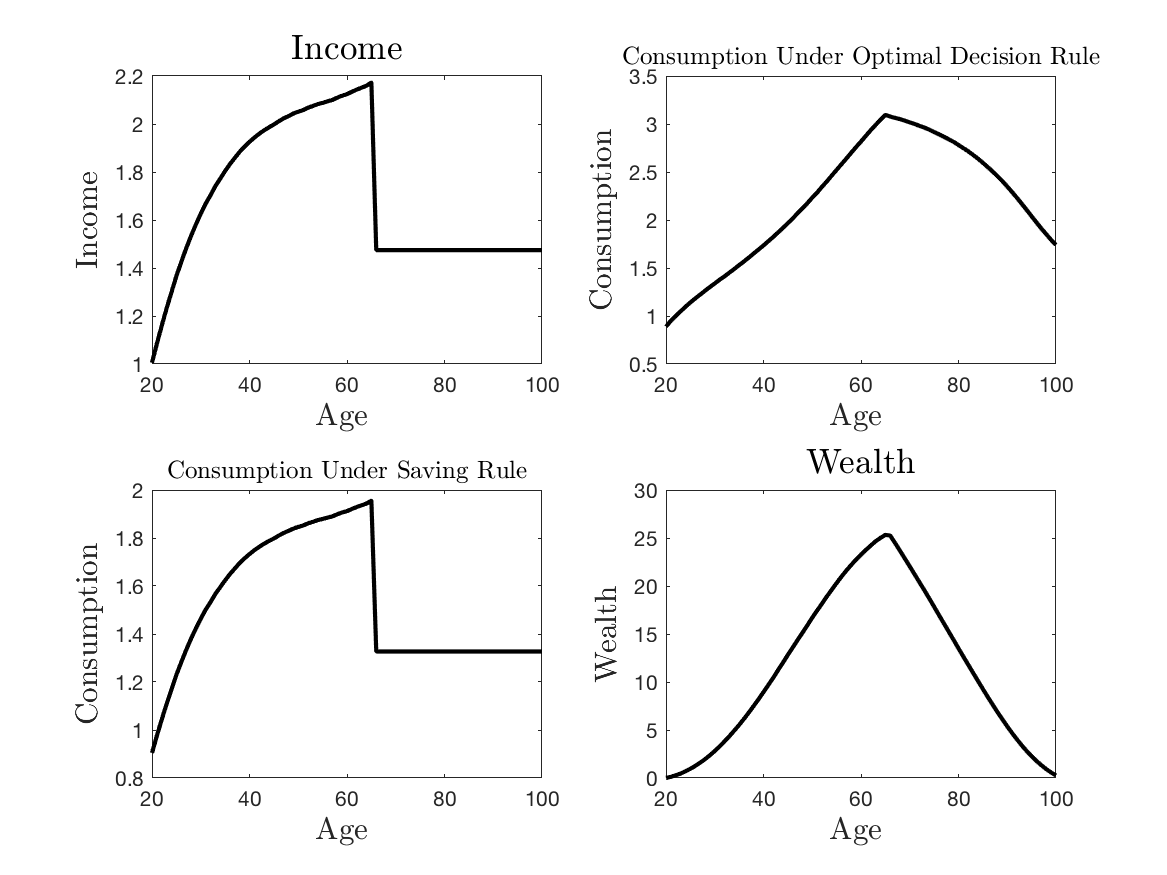

Solving the lifecycle model for standard parameter values gives paths for income, consumption and wealth that look something like this

As the graphs make clear, optimal consumption deviates quite substantially from the heuristic level, smoothly increasing over working life and then smoothly decreasing after retirement.

Personally, I come down somewhere between the two approaches in my own behaviour but come closer to the textbook economic approach. While I can’t claim to have solved the Bellman equation for my own consumption-saving problem, I roughly choose a level of consumption that delivers me a reasonable standard of living rather than targeting a level of saving. Since my current income as a PhD student is (hopefully) much less than what it will be in the future, this means that I likely save less as a fraction of my income than the 10-15% heuristic, but in the future I will likely be saving more than this rate to produce a reasonably smooth consumption path over time. With this being said, I think there is something to be said for the idea that saving is indeed a skill that needs to be developed. In an economic model, the consumer can choose an optimal level of saving and execute it with no cognitive costs, whereas in reality, individuals are of course human beings subject to temptation and imperfect discipline that can be improved with experience when it comes to saving behaviour. The degree to which people really do find saving easier with practice is something that could definitely do with some more empirical testing.

2) Portfolio Allocation

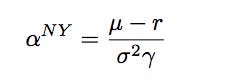

How much of your total wealth should you put in stocks relative to risk-free assets such as bonds or cash? This is an old question in financial economics that goes back at least as far as Merton (1969). The Merton problem features a risk-averse consumer who chooses their consumption and allocates their wealth between a risky asset with normally distributed returns, and a risk-free asset. There is no labour income. The solution is incredibly elegant, and the optimal risky asset share is given by:

Where α is the share of wealth held in risky assets, μ is the mean return on the risky asset, r is the risk-free rate, σ is the standard deviation of the risky asset return and γ is the risk aversion parameter. Note that this solution does not depend on the investor’s age or wealth. It simply states that the investor should multiply the Sharpe ratio on the risky asset (the market portfolio) by the inverse of their risk aversion parameter times the volatility of the risky asset to obtain their risky portfolio share. With a realistic Sharpe ratio of 0.45, a standard deviation of 0.2 and a risk aversion parameter of 4, we can obtain the well-known recommendation that the investor should hold 60% of their wealth in risky assets and 40% in risk-free bonds.

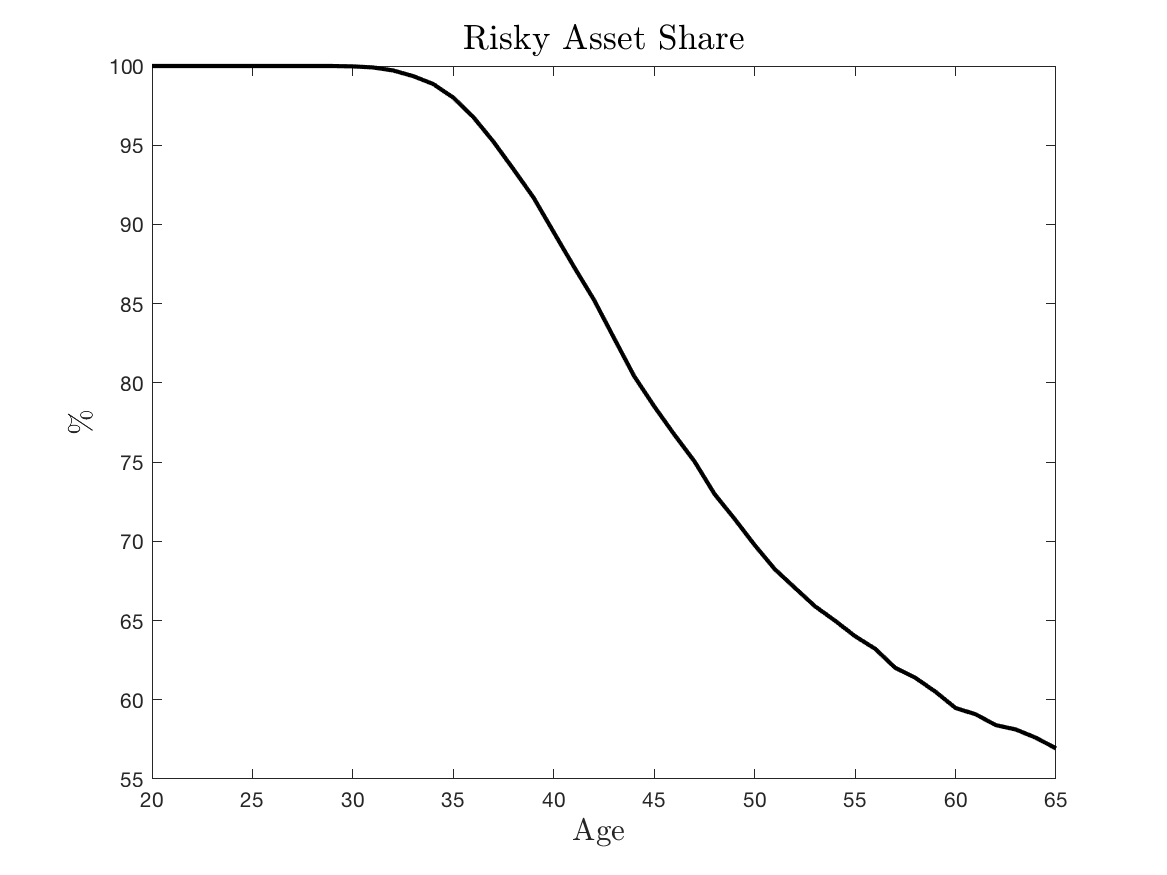

While elegant, the Merton model clearly misses some important features, most notably risky labour income. This is included in the life-cycle problem considered previously, and so we can also plot the optimal equity share over the life-cycle after solving this:

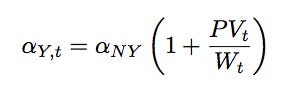

The equity share begins at 100% and stays there until about the age of 35 before slowly declining towards around 60% at retirement. The reason for this is that now the optimal risky asset share can be approximated as:

Where PV is the present discounted value of expected future labour income i.e. human capital. Early in life, financial wealth is low but human capital is high since labour income is expected to be much higher in the future, and as a result, the agent optimises by holding more in stocks when young. As the agent ages, their financial wealth grows and their human capital decreases since retirement looms large resulting in the ratio falling. This means the multiplicative term approaches 1 towards the end of working life and the Merton rule becomes roughly optimal at this stage.

There are many extensions to this benchmark model. Indeed, in my own research, I am currently working on incorporating job loss into the framework, which empirical evidence suggests is associated with a large permanent decline in income. In the life-cycle model above, permanent income shocks are normally distributed which implies that large income increases are just as likely as large income decreases. Job loss introduces negative skewness into the income process, and since young workers are more exposed to this source of risk this can potentially imply that they should actually hold far less in risky assets. Several other papers also alter the framework to produce the result that the risky asset share should be a hump-shaped function of age rather than a strictly decreasing one. For example, Cocco, Gomes, and Maenhout (2005) show that this emerges when stock returns are strongly correlated with labour income. Fagereng, Gottlieb, and Guiso (2017) obtain this result when there is a non-trivial risk of a stock market crash occurring that features a large negative return. As such, it is fair to say that the hump-shaped age profile of the risky share represents something akin to a consensus result in the academic literature.

Interestingly, many personal finance authors provide a similar recommendation but typically for entirely different reasons. The emphasis in these texts is usually on the principle that stocks are safe in the long run, i.e. their Sharpe ratio is an increasing function of the investment horizon. Given that young investors have a long horizon, they should then invest a large fraction of their wealth in stocks. Many authors combine this recommendation with advice to hold a fixed chunk of assets in liquid cash to cover short-term expenses. Fulfilling this requires a large fraction of a young individual's wealth, but this fraction declines as their wealth grows but the amount held in cash is fixed, which ultimately produces a hump-shaped equity share profile. It can be shown that stocks are indeed safer in the long run if their returns are negatively autocorrelated, which in other words means that a bad year is more likely to be followed by a good year than another bad year. This is not something that is supported by much empirical evidence, however. Regressing the yearly returns on the SP500 on one lag of itself yields a coefficient that is slightly positive and not statistically significant, indicative of a lack of negative autocorrelation in the data. It thus seems as if returns are close to serially uncorrelated, as they are in the model considered throughout. Choi finds that:

" Thirty-one of the 45 books that offer some form of asset allocation advice assert that stocks become less risky, and hence more attractive, as the holding period increases. Twenty of these books justify this argument by pointing to the fact that historically, stocks were less likely to underperform fixed-income assets or to have a negative cumulative return as the holding period increased. Twelve books say that stock returns mean-revert; a common saying is that stocks are “on sale” after a large price decline."

No consideration is typically given to existing financial wealth, human capital or risk aversion, which are the key properties that generate the hump-shaped profile in the model. As such, I think this is a case where the prescription of the popular finance gurus is sensible, but their diagnosis is not. As discussed, there are many reasonable features one could include in a portfolio choice model that could generate a range of optimal portfolio allocation decisions, but these need to be grounded in empirical reality. This is not the case for the logic used by many of the authors and I think their advice regarding the issue is not particularly worth paying attention to for this reason.

Top 10s of 2022

I have always been a big fan of end-of-year lists as a way of documenting the year in popular culture. Hopefully you enjoy some of these recommendations.

TV Shows

A very good year for TV I would say. Throughout, I always felt there was more I would like to watch, which perhaps speaks to the depth of quality shows out there. I did not get around to watching Severance, The Bear, Black Bird or This is Going to Hurt, although I would have liked to, and hence their absence on the list. I also have never watched Better Call Saul which I realise is a serious omission on my part.

Honourable mentions: Cheer (S2), Industry (S2), Under the Banner of Heaven

Ozark (S4)

A pretty satisfying end to a good show. The ending wasn’t perfect, but few endings are.

The Dropout

An interesting and entertaining look at the Theranos scandal. Amanda Seyfried is superb as Elizabeth Holmes, and deserves all the plaudits.

Andor

Much better than the other Disney shows apart from The Mandalorian. It had no right to be as good as it was, and there are a couple of episodes (namely episodes 6 and 10) that were amongst the best of the year.

Sherwood

A well-written look at the inter-generational transmission of bad blood stemming from the mining strikes of 1984. It could easily have been a polemic in the wrong hands, but James Graham did a great job here.

Conversations with Friends

This is perhaps a controversial one as I know many people did not like this show, but personally I found it to be almost as good as Normal People.

Slow Horses (S1)

I love spies and so was a mark for Slow Horses. It isn’t your traditional espionage show however, with a few curveballs thrown in. A lot of it was filmed in Barbican very close to where I used to live.

The Staircase

I had not watched the documentary of the same name and so did not know much about the absolutely bizarre story. This show is gripping throughout, and not enough can be said about Toni Collette’s performance.

Euphoria (S2)

Not to everyone’s taste, but I found it wildly entertaining. A rare 2022 show that captures the cultural zeitgeist to any meaningful extent, and I found myself looking forward to every episode each week.

House of the Dragon

I was worried that this would be a real flop, but I was wrong thankfully. Being back in the GOT world was more enjoyable than I anticipated, and the degree of difficulty in adapting a pseudo-history that covers a large period of time cannot be understated. The scene where King Viserys drags himself through the throne room was brilliant and up there with the best moments of the GOT series.

The White Lotus (S2)

I liked the first series of The White Lotus very much, but it pales in comparison to how good the second series is. Mike White is a genius who has created something so rich in detail whilst not straying into the realm of cliche. Worth watching for the Sicilian setting alone.

Films

I have really been slacking this year when it comes to watching films. I think this is in large part due to the fact that it hasn’t been a particularly good year for them. Irritatingly, many of the awards contenders such as Tar and The Fabelmans are not released until 2023 in the UK and so frustratingly I have not had a chance to see them yet, although am looking forward to doing so. Due to my lack of viewing, I will do a top 5 list.

Honourable mentions: Turning Red, The Northman, The Batman

Nope

I must admit I’m not entirely sure how I feel about Nope. It has some great sequences in and I think it is cleverly constructed. Does it work cohesively as a film? I’m not sure, but I did really enjoy it.

Glass Onion: A Knives Out Mystery

I loved the first Knives Out, and the sequel is 85% as good which still makes it a good watch. I was a little concerned after the first half an hour that it would be a dud, but the film turns it around in the second half. Looking forward to re-watching it when it comes out on Netflix over Christmas.

The Banshees of Inisherin

In Bruges is one of my favourite films and so I was always going to be positively predisposed to its spiritual sequel. Not everything about it works, but I found it to be a well crafted look at male friendship and existential crisis.

The Souvenir: Part II

Likewise, I loved part one of The Souvenir and the sequel is really a continuation of Joanna Hogg’s quasi-autobiographical story of a film school student who is dealing with rather a lot. Just like part one, part two is quite beautiful.

Top Gun: Maverick

Good lord, what a film. I have seen this mutlipleF times now and will watch it again over Christmas. It made $1.5 billion at the box office, and I cannot describe how deserved this is. Kosinski did a great job making this, and Tom Cruise is almost singlehandedly carrying the movie industry at this point. It truly isn’t the plane, it’s the pilot.

Albums

A really fantastic year for music in my opinion, with a lot of top tier releases. Narrowing these down to ten was not easy, which I suppose is indicative of the depth this year had to offer. This is reflected in the high number of honourable mentions.

Honourable mentions: Rosalia - Motomami, The 1975 - Being Funny in a Foreign Language, Rachika Nayar - Heaven Come Crashing, Florist - Florist, MJ Lenderman- Boat Songs, Destroyer- LABYRINTHITIS, Beach House- Once Twice Melody, The Weeknd - Dawn FM.

Nilüfer Yanya - PAINLESS

A great indie-pop album with many standout tracks, the best of these being The Dealer and Midnight Sun.

The Smile - A Light For Attracting Attention

Just as good as many Radiohead albums for the most part. I saw them live at the Camden Roundhouse in June which was terrific. The best songs are You Will Never Work in Television Again and Free in the Knowledge.

Kendrick Lamar - Mr Morale & The Big Steppers

It seems as if this album is destined to become underrated unfortunately, which is a shame since it is still fantastic while not being as good as good kid, M.A.A.D, city or To Pimp a Butterfly. Ironically, Kendrick’s best song this year was The Heart Part 5 which isn’t actually on the album, but there are many strong tracks on here such as N95 and Mother I Sober.

SZA - SOS

I’m wary of recency bias on this one, since it only came out a week or so ago, but I do think it is deserving of this spot nonetheless. While there is some filler amongst the 23 tracks, there is not as much as you might have expected and there aren’t many obvious skips amongst them. Highlights are Kill Bill, Open Arms, Ghost in the Machine, and Nobody Gets Me.

Black Country, New Road - Ants From Up There

I thought this may end up being my favourite album of the year when it came out, and the fact it is not speaks to the quality of other LPs released since. Some find the band obnoxious, which I can understand, but I find their uniquely melodramatic brand of post-punk to be quite addictive, frankly. A great shame that Isaac Wood has left the band. Best songs are The Place Where He Inserted the Blade, Good Will Hunting and Basketball Shoes.

Big Thief - Dragon New Warm Mountain I Believe in You

Another album that came out in Febrauary which I would have anticipated being higher on the list. Nonetheless, a brilliant indie/folk album with a nice diversity of songs on it. Standouts for me are Little Things, Certainty, Spud Infinity, No Reason, and Simulation Swarm.

Alvvays - Blue Rev

It took a few listens for this to fully grow on me, but after it did I really loved it. Very consistent front-to-back, there are not any bad songs on here. Belinda Says is one of the best songs of the year, and Pharmacist, Easy on Your Own and Velveteen are all very good also.

Bad Bunny - Un Verano Sin Ti

Just a great summer record that has a lot of earworms on it. I can’t say I had listened to Bad Bunny much before this album, but this one clicked for me. Perhaps a little on the long side, but like the SZA album there isn’t too many bad songs on here and there are many good ones. Best tracks are Neverita, Ojitos Lindos, Otro Atardacer, and Enséñame a Bailar.

Beyoncé - Renaissance

Beyoncé’s best album in my opinion, although there are many great ones to choose from. A completely different sound to her previous work which blends house music and other dance genres like ballroom to great success. Standout tracks are Cozy, Cuff it, Heated, Break My Soul, Virgo’s Groove and Move.

Alex G - God Save the Animals

My most listened to album this year and it probably was not particularly close. A beautiful set of tracks that is just so sweet on the ear, which is what I seem to have a strong preference for. Runner is a fantastic song, and my other favourites include Mission, Cross the Sea, Miracles, Forgive and Blessing.

That’s all from me in 2022 and I will be back writing in 2023. Thank you to all of you who read and subscribe to the newsletter, I really do appreciate it. Have a great Christmas and a happy new year - Andy.

I think it's correct to say that stocks (and all assets) are less risky as T gets large under most useful definitions of risk. For example, as T gets large (assuming avg return on stocks is 6%) the probability of losing money goes to zero, as does the probability of losing to a lower-return asset. For most people this means its pretty low risk to invest in stocks long-term. Obviously the variance of total returns does grow (assuming no neg. autocorrelation), but the average annual returns converges to the 'true' expected annual return of the asset.

Standard utility functions seem lacking. People get utility from more than just consumption. To get a realistic utility function, I'd propose the following changes.

The utility function should depend on savings rates, wealth, and work-based income in addition to consumption. People get utility from a high savings rates, especially at low wealth levels. And that diminishes as wealth increases. People get disutility from work (proxied by work-based income), and the disutility rises as wealth rises.

These change reflect real world preferences. Young people enjoy saving a lot of money because young people are unsure of their future earnings potential, and they're used to low consumption. Plus, consuming a lot before you've "earned" the right to consume a lot feels immoral. As people become wealthier, they are less concerned with saving money, and are more willing to spend. And as people become wealthier, they are less interested in paid work. What do you think?